Will Insurance Replace an Old Roof? What You Should Know

If your roof has taken a beating from Ohio's storms and you're wondering how to get insurance to pay for roof replacement, you're not alone—and you're not out of options. The short answer: yes, homeowners insurance can cover a full roof replacement, but only if the damage was caused by a covered event and you follow the right process. Miss a step, and you risk a denied claim or a payout that barely scratches the surface.

Key Takeaways

- Homeowners insurance covers roof replacement caused by sudden events like storms, hail, wind, or falling trees—not normal aging or neglect.

- How much you receive depends on whether your policy pays Replacement Cost Value (RCV) or Actual Cash Value (ACV).

- Proper documentation—photos, dates, contractor inspection reports—is the single biggest factor in whether a claim gets approved or denied.

- A licensed roofing contractor who understands the insurance process can make or break your claim outcome.

I've been roofing homes in Central Ohio for years, and one of the most common calls I get after a storm isn't "can you fix my roof?"—it's "will my insurance cover this?" The answer isn't always simple, but I've helped dozens of Pickerington homeowners navigate this process and come out the other side with new roofs they didn't have to pay for entirely out of pocket.

This guide is everything I wish every homeowner knew before they picked up the phone to call their insurance company. Whether you're dealing with hail damage, wind damage, or an aging roof that finally gave out, I'm going to walk you through exactly how to get insurance to pay for roof replacement—and what to do if they push back.

Does Homeowners Insurance Cover Roof Replacement?

Yes, homeowners insurance typically covers roof replacement—but only when the damage is caused by a covered peril, not gradual deterioration. Most standard policies protect against wind, hail, fire, lightning, and falling debris like tree limbs. What they don't cover is a roof that's simply worn out from years of weathering Ohio's freeze-thaw cycles.

What Counts as a Covered Peril in Ohio?

Ohio homeowners face some of the most unpredictable weather in the Midwest. Covered events typically include:

- Hailstorms — Hail damage is one of the most common reasons Central Ohio homeowners file roof claims. Even quarter-sized hail can crack shingles and compromise the granule layer that protects against UV damage.

- Wind damage — High winds can lift, curl, or strip shingles entirely. If you lose even a few shingles in a storm, water can get into the decking fast.

- Fallen trees or branches — Impact damage from a storm-blown tree is typically covered, regardless of whose tree it was.

- Fire or lightning strikes — Less common but fully covered under most standard policies.

What Insurance Won't Cover

Here's where I see a lot of homeowners get tripped up. Insurance is not a maintenance plan. Policies almost universally exclude:

- Roof aging or gradual wear and tear

- Moss, algae, or mold buildup from neglect

- Cracked or curling shingles from years of sun exposure

- Poor original installation or low-quality materials

"I tell every homeowner I meet: insurance is there for the unexpected. If your roof is leaking because it's 25 years old and nobody's touched it since Clinton was president, that's a maintenance issue, not an insurance issue. But if a storm rolls through Pickerington and takes out half your shingles? That's exactly what your policy is for." — Will Price, Price Brothers Restoration

Will Insurance Cover a 20-Year-Old Roof?

Possibly—but your payout may be significantly lower than you expect. The age of your roof is one of the first things an insurance adjuster looks at when evaluating a claim, and it directly affects how much you receive.

How Roof Age Affects Your Payout

Most insurers break roof coverage into tiers based on age:

- Under 10 years old: Likely covered at full replacement cost if damage meets the threshold.

- 10–20 years old: Many insurers offer partial reimbursement based on depreciation. You may receive 50–70% of replacement cost.

- 20+ years old: Most policies shift to Actual Cash Value (ACV) only, which factors in depreciation heavily. ACV policies typically depreciate roofing materials at 3–5% per year Paccsolutions, meaning a 20-year-old roof might receive a fraction of what a new one would cost.

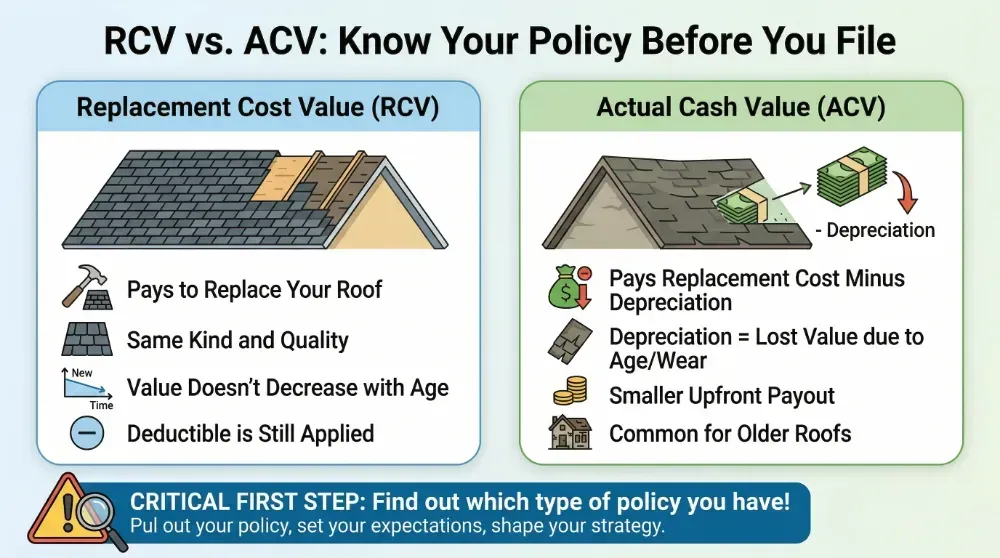

RCV vs. ACV: Know Your Policy Before You File

Replacement Cost Value (RCV) pays to replace your roof with the same kind and quality after repairs are completed, minus your deductible—you don't lose value just because your roof is older. Actual Cash Value (ACV) pays the replacement cost minus depreciation upfront, which can mean a much smaller immediate payout for an older roof. Paccsolutions

Before you file anything, pull out your policy and find out which type you have. This one detail will set your expectations and shape your entire strategy.

How Does Roof Age Affect Homeowners Insurance Rates?

A newer roof typically lowers your homeowners insurance premium because it represents lower risk to the insurer. Insurance companies sometimes offer only actual cash value coverage on roofs over a certain age, which means your out-of-pocket costs will be higher when a claim occurs. Insurance.com Installing a new roof—especially a Class 4 impact-resistant shingle—can reduce your annual premium in some cases, making the replacement investment work double duty.

Will a New Roof Lower My Insurance?

In many cases, yes. Most major insurers reward newer roofs with lower rates, particularly if you upgrade to materials rated for hail or wind resistance. If you're on the fence about replacing an aging roof, the long-term premium savings are worth factoring into your decision alongside the upfront cost.

How to Get Insurance to Pay for Roof Replacement: Step by Step

This is the process I walk my Pickerington customers through every time we work on an insurance-involved replacement. Following these steps in order dramatically improves your odds.

Step 1: Document Everything Before You Touch Anything

The moment you notice damage—whether it's right after a storm or the next morning—start documenting. Take clear, timestamped photos of every affected area: missing shingles, dented flashing, granule accumulation in gutters, and any interior water stains on ceilings or walls. Record the date and time of the event, and save weather reports or news articles confirming the storm, so you can clearly demonstrate the link between the damage and the covered event. Rcaw

Don't wait. Most insurance policies require claims to be submitted within 30 to 60 days following the damage Cobexcg, and delays can be used to justify a denial.

Step 2: Get a Professional Roofing Inspection

Before you call your insurance company, call a licensed roofing contractor. A professional inspection gives you an independent, documented assessment of the damage that carries real weight with insurance adjusters. Most adjusters are generalists, not roofing specialists—a qualified contractor can identify subtle damage that an adjuster might miss Mighty Dog Roofing, which means more of the damage gets counted toward your claim.

At Price Brothers Restoration, our Pickerington roofing inspections include detailed written reports formatted specifically to support insurance claims.

Step 3: Review Your Policy and File Promptly

Before filing, review your policy for your deductible amount, whether you have RCV or ACV coverage, and any specific exclusions for older roofs or certain types of damage. Then file your claim with all documentation attached—photos, contractor inspection report, storm date, and a factual description of the damage. Keep copies of everything you send.

"One thing I always tell people: stick to the facts when you file. Document what happened, when it happened, and what the damage looks like. Don't speculate, don't guess at causes. Let the evidence speak for itself." — Will Price, Price Brothers Restoration

Step 4: Be Present for the Adjuster's Inspection

Once you file, your insurance company will send an adjuster to inspect the damage. Be there. Walk the entire roof with them and point out every area your contractor identified. Having your roofing contractor present during this inspection is one of the highest-leverage moves you can make. Clearly communicate how the damage impacts your home to justify the need for a full roof replacement, and ensure the adjuster thoroughly inspects all areas, not just easily visible ones. Storm Law Partners

Step 5: Review the Settlement Offer Carefully

Once the adjuster submits their report, the insurer will issue a settlement offer. Review it line by line against your contractor's estimate. If the numbers don't match, ask for an itemized breakdown. Insurers sometimes miss storm-related damage or undervalue scope of work—and you have the right to push back.

What to Do If Insurance Denied Your Roof Claim

A denial is not the end of the road. About 40% of roof claims are denied annually Paccsolutions, and many of those denials can be successfully appealed—especially when the denial is based on inadequate documentation rather than a genuine policy exclusion.

How to Appeal a Denied Roof Claim

- Request the denial in writing — The insurer must specify exactly why the claim was denied.

- Get a second professional inspection — A second roofing report from a licensed contractor can directly counter the adjuster's findings.

- Gather additional evidence — Local weather service data, radar records, and NOAA storm reports can corroborate the timing and severity of a weather event.

- Submit a formal appeal — Resubmit your claim with the new documentation and a written letter addressing each denial reason specifically.

- Consider a public adjuster — A public adjuster works on your behalf, not the insurer's, and takes a percentage of the final settlement. For complex or large claims, this can be worth it.

"I've seen claims come back from denial when the homeowner had the right documentation the second time around. It's not over until it's really over. Don't just accept a denial—understand why it happened and decide if it's worth fighting." — Will Price, Price Brothers Restoration

How Do Roofing Companies Work With Insurance Companies?

A good roofing contractor isn't just someone who nails shingles—they're your partner through the entire claims process. At Price Brothers Restoration, we regularly work alongside insurance adjusters to make sure every inch of storm damage gets properly assessed and documented. We understand what adjusters look for, how to write inspection reports that insurers accept, and how to communicate scope-of-work in a way that reduces back-and-forth.

According to the Insurance Information Institute, working with a licensed contractor during the claims process is one of the most effective ways to protect your interests. And the National Roofing Contractors Association emphasizes that professional inspections from credentialed contractors carry far more weight with insurers than homeowner self-assessments.

For homeowners in Pickerington, Reynoldsburg, and surrounding Central Ohio communities, our team guides you through the entire insurance-assisted roof replacement process—from that first inspection call all the way to the final shingle.

Does a New Roof Lower Homeowners Insurance?

Yes, in most cases a new roof will reduce your homeowners insurance premium—sometimes significantly. Insurers view newer roofs as lower risk because they're less likely to fail, leak, or suffer storm damage that leads to costly claims. Impact-resistant roofing materials, rated Class 3 or Class 4, can earn even steeper discounts with many carriers.

If you're already facing a partial or full replacement, it's worth asking your insurance agent about potential premium savings after the new roof is installed. In some cases, those annual savings can offset a meaningful portion of any out-of-pocket costs you paid.

FAQ: Roof Replacement and Insurance Coverage

Will homeowners insurance pay for a 20-year-old roof?

Most insurers will cover storm damage to a 20-year-old roof, but the payout will likely be based on Actual Cash Value (ACV) rather than full replacement cost, meaning depreciation will reduce your check. Some carriers won't offer RCV coverage on roofs over 15–20 years at all.

Does homeowners insurance cover a leaking roof?

It depends on the cause. If the leak resulted from storm damage—a broken shingle after a hailstorm, for example—it's likely covered. If the leak is from gradual deterioration or lack of maintenance, most policies will deny the claim.

Does home insurance cover wind damage to a roof?

Yes, wind damage is a covered peril under most standard homeowners policies. Ohio's severe weather season makes wind claims among the most common in Central Ohio. Document the damage quickly and file promptly.

Do insurance companies cover metal roofs?

Yes. Metal roofs are covered under most homeowners policies and may even qualify for lower premiums due to their durability and longevity. Some insurers offer specific endorsements for impact-resistant metal roofing.

What if my insurance company only offers a partial settlement?

You can negotiate. Provide your contractor's full estimate, any supplemental documentation, and a written response explaining the discrepancy. If the gap is significant, consider hiring a public adjuster to advocate on your behalf.

Ready to File a Roof Insurance Claim in Pickerington?

Knowing how to get insurance to pay for roof replacement starts with one thing: taking the right steps in the right order. Document the damage immediately, get a professional inspection, file your claim promptly, and don't accept a denial without first understanding why.

At Price Brothers Restoration, we've helped homeowners across Pickerington, Reynoldsburg, and Central Ohio navigate this process and get roofs replaced with minimal out-of-pocket cost. We show up to adjuster inspections, write inspection reports built for insurance review, and stand behind our work long after the last shingle is down.

If you've had storm damage—or even if you're just not sure—reach out to our Pickerington roofing team for a free inspection. We'll give you an honest assessment, help you understand your coverage options, and be with you every step of the way.